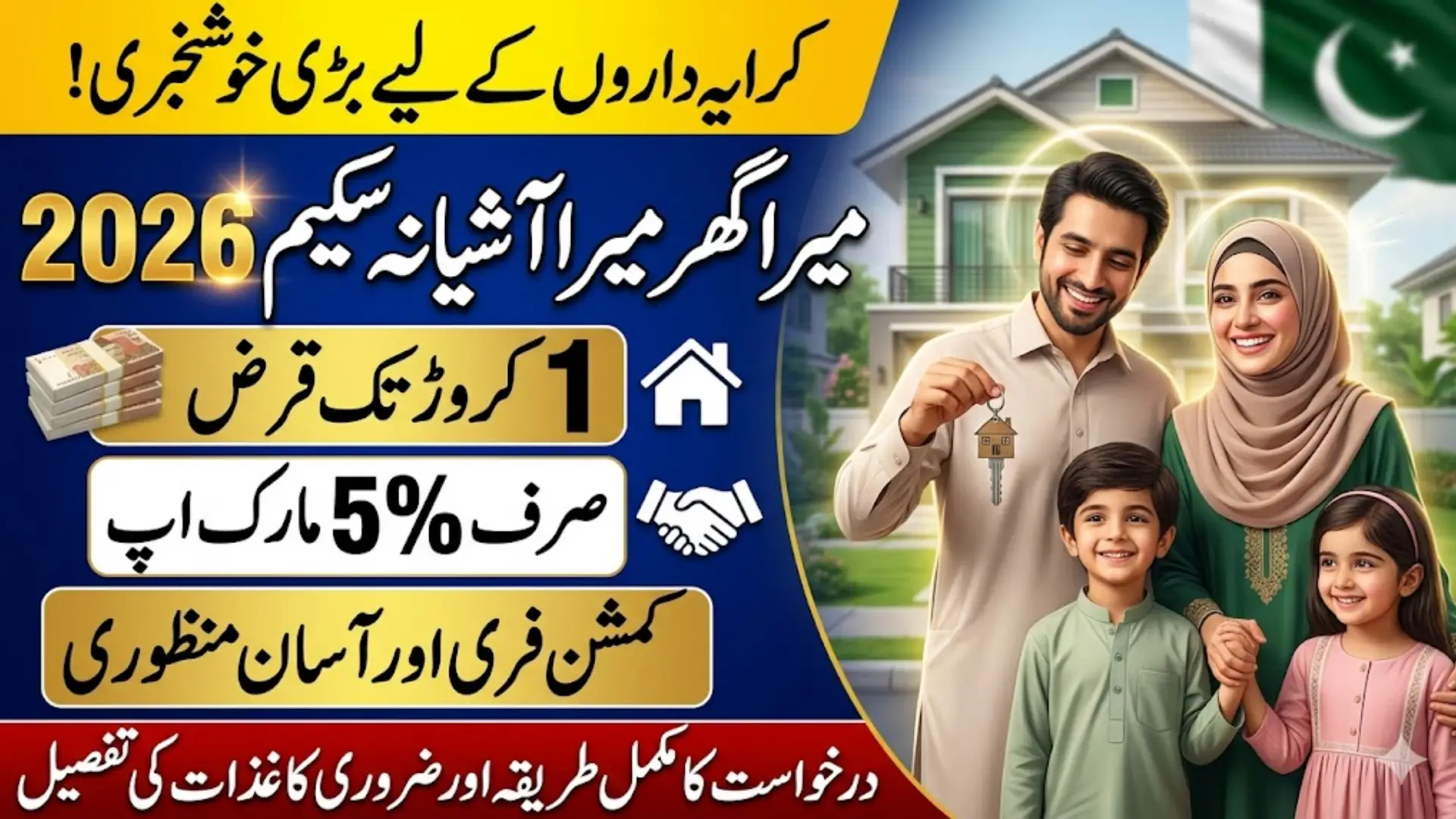

Mera Ghar Mera Ashiana Scheme 2026

Mera Ghar Mera Ashiana Scheme 2026 In Pakistan, owning a house has become one of the biggest challenges for middle-class families. Property prices have increased sharply in recent years, and rent is also rising in almost every city. Many people spend a large portion of their income on rent, but still cannot save enough to buy their own home. This situation has created strong demand for government-backed housing schemes that can actually work on the ground.

The Mera Ghar Mera Ashiana Scheme 2026 is being seen as a practical solution because it focuses on affordability and accessibility. This time, the government has made real improvements such as lower markup, easier bank procedures, and a higher loan limit. From what is being observed, people are more confident in applying because the scheme now feels realistic instead of just a policy announcement.

Major 2026 Changes That Make This Scheme More Practical

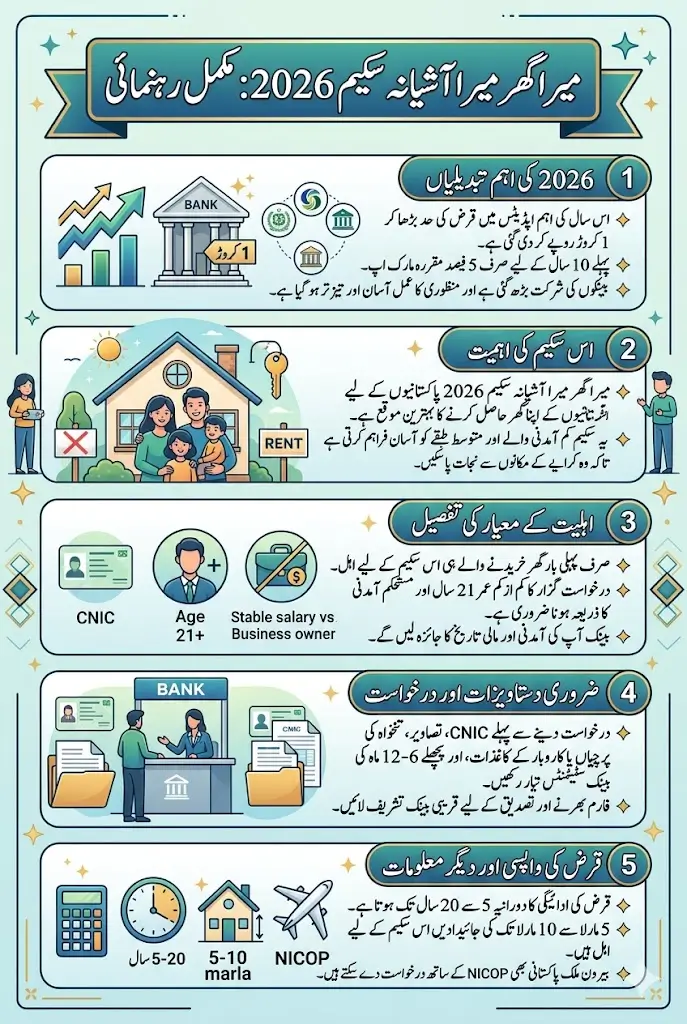

The latest version of this scheme comes with several updates that directly address the problems faced by applicants in previous years. The most important change is the increase in the loan limit up to 1 crore rupees, which allows families to choose better housing options without being restricted to very small or low-quality properties. This change alone has made the scheme more flexible and appealing.

Another major improvement is the fixed markup of 5% for the first 10 years. Earlier, people were worried about rising interest rates, but now the subsidy ensures stable and manageable monthly installments. In addition, more banks are now part of the program, which means applicants have more choices and faster processing times. This wider participation also reduces pressure on a few banks and improves overall efficiency.

Key highlights of 2026 update:

- Loan limit increased up to Rs. 1 crore

- Fixed 5% markup for first 10 years

- Wider bank participation across Pakistan

- Easier and faster approval process

- Improved access for middle-income families

Eligibility Criteria Explained in Simple Words

This scheme is specially designed for individuals who do not own any house. The government wants to support those families who are still living in rented homes and struggling to manage their expenses. If a person already owns a property, they will not be eligible for this scheme, as the focus is on first-time home buyers.

Applicants must be Pakistani citizens and should have a valid CNIC or NICOP. The minimum age requirement is 21 years, which ensures that the applicant is financially responsible. Salaried individuals can apply until their retirement age, while business owners are allowed up to 65 years. These conditions are designed to ensure that the applicant can repay the loan without difficulty.

Basic eligibility requirements:

- Must be a first-time home buyer

- Valid CNIC or NICOP required

- Minimum age is 21 years

- Stable income source is necessary

- Must meet bank’s financial checks

Income Requirements and Bank Evaluation Process

Banks play a key role in approving housing loans, and they carefully review each applicant’s financial condition. The main purpose of this evaluation is to confirm whether the applicant can pay monthly installments regularly. Without a stable income, it becomes difficult to get approval, even if all other documents are complete.

In most cases, applicants need a monthly income starting from around 25,000 to 50,000 rupees or more, depending on the loan size. Higher income increases the chances of approval and allows access to a larger loan amount. Banks also check your transaction history, existing loans, and overall financial discipline before making a final decision.

Important financial factors banks consider:

- Monthly income consistency

- Previous banking history

- Existing loans or liabilities

- Savings pattern and expenses

- Job stability or business continuity

Step-by-Step Method to Apply for Housing Loan

The application process is straightforward, but many people face problems because they are not properly guided. The first step is to visit a participating bank and request the housing loan form. It is very important to fill out this form carefully because even small mistakes can cause delays.

After submitting the form, the bank reviews your documents and financial record. They also verify the property you want to purchase or construct. Once everything is approved, the loan is released in stages, especially in the case of construction. This ensures proper use of funds and reduces risk for both the bank and the applicant.

Application process steps:

- Visit nearest participating bank

- Collect and fill application form

- Attach all required documents

- Submit form for verification

- Wait for approval and disbursement

Complete List of Documents You Need Before Applying

One of the most common reasons for delays is missing or incomplete documents. Many applicants visit banks without proper preparation, which results in repeated visits and frustration. It is always better to prepare all required documents in advance to avoid unnecessary delays.

You will need your CNIC copy, passport-size photographs, and proof of income. Salaried individuals should bring salary slips and job letters, while business owners need to provide NTN and business-related documents. Bank statements for the last 6 to 12 months are also required to check your financial activity.

Documents checklist:

- CNIC copy

- Passport-size photographs

- Salary slips or business proof

- Bank statements (6–12 months)

- Utility bills

- Property-related documents

Loan Repayment Plan and Installment Details

The repayment structure of this scheme is designed to make it easier for borrowers in the initial years. The loan duration can range from 5 to 20 years, depending on your financial capacity and agreement with the bank. The most beneficial part is the fixed 5% markup during the first 10 years, which keeps monthly installments affordable.

After the first 10 years, the bank’s standard interest rate will apply. However, by that time, a significant portion of the loan is already paid off, so the financial burden becomes lighter. This structure is helpful for families who want to manage their expenses without stress in the early years.

| Loan Feature | Details |

|---|---|

| Maximum Loan | Up to Rs. 1 Crore |

| Markup Rate | 5% (First 10 Years) |

| Loan Duration | 5 to 20 Years |

| Installments | Monthly |

| After 10 Years | Bank Standard Rate Applies |

Common Mistakes That Lead to Rejection

Despite meeting basic requirements, many applicants get rejected due to avoidable mistakes. One major issue is applying without proper income proof. Banks need clear and verifiable evidence that you can repay the loan, and without it, approval becomes difficult.

Incomplete forms and incorrect information also create serious problems. Some applicants select properties that do not meet scheme criteria, such as incorrect size or legal issues. These mistakes can delay or completely cancel the application process.

Common mistakes to avoid:

- Submitting incomplete documents

- Providing incorrect information

- Weak or unstable income proof

- Choosing ineligible property

- Ignoring bank requirements

Expert Advice to Improve Loan Approval Chances

From practical experience, applicants who prepare properly have a much higher chance of success. Maintaining a clean banking history is one of the most important steps. Avoid late payments, unpaid loans, or financial irregularities before applying for the scheme.

It is also advisable to choose a property within your financial limit. Applying for a smaller loan increases approval chances and reduces long-term pressure. Clear communication with bank staff can also help you understand the process better and avoid mistakes.

Tips for better approval chances:

- Keep banking record clean

- Avoid loan defaults

- Choose affordable property

- Prepare documents in advance

- Consult bank officials before applying

Property Rules and What You Must Know Before Selection

The scheme allows both purchasing and constructing a house, but there are specific limits. Typically, properties between 5 to 10 marla are considered eligible. This ensures that the scheme benefits middle-income families rather than luxury property buyers.

Banks also verify the legal status of the property before approving the loan. If there are any legal complications, your application can be rejected. It is always recommended to check all documents carefully before finalizing any property.

Processing Time and What Happens After Approval

After submitting your application, the approval process usually takes around 3 to 6 weeks. This timeline can vary depending on how complete your documents are and how quickly the bank completes its verification process. In some cases, delays happen due to missing information or legal issues.

Once the loan is approved, the amount is released in stages, especially for construction projects. Monthly installments start according to the agreed plan. Staying in contact with your bank during this period helps you stay updated and avoid confusion.

Opportunities for Overseas Pakistanis in This Scheme

Overseas Pakistanis can also take advantage of this housing scheme if they have a valid NICOP. This is a great opportunity for those who want to invest in property in Pakistan and secure a home for their family. The process is mostly similar, but additional documents related to foreign income may be required.

Proper planning and documentation can make the process smooth for overseas applicants. Many banks are now facilitating overseas Pakistanis, which makes this scheme even more accessible.

Final Thoughts

The Mera Ghar Mera Ashiana Scheme 2026 is one of the most practical housing options currently available in Pakistan. With features like low markup, higher loan limits, and easy bank access, it provides real support to families who want to own a home instead of living on rent.

If you meet the eligibility criteria, it is a good idea to start preparing your documents and apply as early as possible. This scheme has the potential to change the lives of many families by turning the dream of home ownership into reality.